Bank of England hints financial ache felt by many to be a protracted, drawn-out affair

Higher for longer.

The Bank of England might have lifted rates of interest by lower than lots of people had been anticipating up till not too long ago – up by a quarter percentage point rather than a half – however for these with mortgages, probably the most hanging factor from the trove of research they’ve revealed right this moment is not about right this moment however about tomorrow.

Because there are heavy hints dropped all through the Bank’s Monetary Policy Report that it expects borrowing prices to remain excessive for lots longer than many had anticipated.

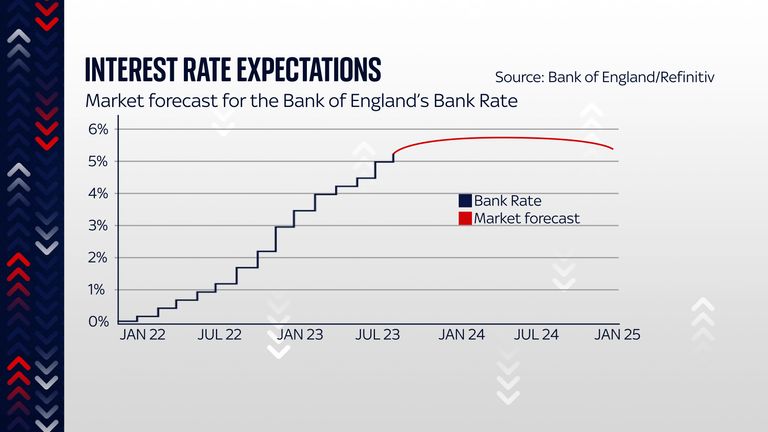

Only a number of months in the past monetary markets had been betting that the Bank Rate – the official borrowing degree set at Threadneedle Street – could be all the way down to 4% by 2024 and three.7% by 2025. Far larger than the post-financial disaster interval however a fall all the identical.

Now, those self same markets suppose charges will nonetheless be at 5.9% in 2024 and at 5% by 2025. And moderately than difficult these assumptions, the Bank has come as shut as attainable to reinforcing them.

This establishment does not present express steerage about the place it is anticipating rates of interest to go; it prefers to drop hints. And the trace within the minutes alongside the choice right this moment was about as heavy as you might get.

“The [Monetary Policy Committee] would ensure that Bank Rate was sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with its remit.”

Higher for longer, in different phrases.

Why? Another clue is to be discovered elsewhere within the Bank’s forecasts right this moment. It’s value quoting at size: “Sharp will increase in power, meals and different import costs over the previous two years have had second-round results on home costs and wages.

“These second-round effects are likely to take longer to unwind than they did to emerge and the Monetary Policy Committee has placed weight in its recent forecasts on the risk that they might persist for longer.

“The committee now judges that a few of this danger might have begun to crystallise.”

‘Interest charges should not happening anytime quickly’

It fears, in different phrases, that the inflation cat is now out of the bag. And thus getting worth rises to come back down might contain significantly extra work on its half than it beforehand anticipated. Higher for longer.

Which in fact means ache for a lot of households – particularly these with mortgages and people renting (most landlords even have mortgages).

And in contrast to earlier eras the place most households had been on floating charge mortgages and thus that ache was in a short time felt of their pockets, right this moment that ache is being drip fed into the economic system as two and 5 yr fixed-rate mortgages progressively expire and are changed with far costlier month-to-month funds.

Read extra from enterprise:

Why renters are more vulnerable to interest rate rises

Effects of interest rate hikes pushing economy towards ‘recession’

The squeeze on renters is a symptom of Britain’s housing crisis

Again, meaning the impression of those rate of interest will increase goes to be a protracted, drawn-out affair. And you may see the implications within the Bank’s financial forecast. The economic system is not prone to face a recession, at the least based on its central projection.

But it’ll basically flatline – depressed by these larger charges – for 3 years, not displaying significant development till 2026.

It is a miserable prospect. Perhaps the perfect factor to hope for is that the Bank is unsuitable. This has occurred earlier than – certainly it is already submitting to an unbiased inquiry into the way it did not foresee the current spike in inflation, led by former Federal Reserve chairman Ben Bernanke.

It’s not altogether implausible that they fail to foresee a extra significant financial restoration.